OK, technically, JPMorgan’s annual ETF extravaganza was actually published late last month. A lot can happen in a month, such as one of the authors sadly departing the bank since publication.

But the 1/4 of Alphaville that cares about the subject was on book leave at the time, and there’s plenty of good stuff to chew on in the 20th edition of the annual snapshot of the ETF industry.

The headline is that the global ETF industry’s assets have grown by ca $3tn since the last report, thanks to ongoing massive inflows and rising markets. That’s more than the total market cap of the FTSE 100, or about one Nvidia these days.

Most of all though, the report highlights how ETFs are becoming a far more diverse and complex ecosystem. That is particularly true in the US, where a 2019 ETF rule has triggered a wild bout of spaghetti-flinging financial masturbation innovation.

While most money continues to flow into classic, vanilla passive funds, the proliferation of thematic ETFs, factor ETFs, multi-asset ETFs, active ETFs and derivatives-based ETFs is accelerating. As JPM’s Marko Kolanovic and Bram Kaplan write:

. . . For the fourth consecutive year, a majority of new ETFs are actively managed. Additionally, managed risk/defined outcome, factor, call/put writing, and thematic funds remained significant areas of focus for issuers over the past year, together accounting for nearly half of all new ETF launches. Cryptocurrency ETFs were another major area of focus over the past year; they accounted for ~5% of new fund launches, and attracted over 40% of the AUM in newly launched funds over the past year.

Active ETFs

The growth of actively managed ETFs has been particularly strong, as more asset managers use the wrapper for new funds, converting old funds, or as a share class of existing funds.

JPMorgan estimates that actively managed ETFs have accounted for over 60 per cent of all US ETF launches every year since 2020. Their assets have grown by about 70 per cent over the past year to reach ca $670bn. Indeed, over the past year they accounted for a quarter of all US ETF inflows.

As JPMorgan points out, this isn’t really denting the broader move into passive investment strategies — whether in mutual fund or ETF wrappers. Rather, active ETFs are merely nibbling at the market share of the mutual fund structure.

Interestingly, there seems to be little interest in less transparent ETF structures, which many thought would be best for active managers that didn’t want to broadcast their trades in near-realtime.

Adoption of the non- and semi-transparent structures remains relatively slow 4+ years after their launch, with just ~$10.7 Bn AUM in total in these funds, accounting for less than 2% of the total AUM in actively managed ETFs. Additionally, a few ETFs that were launched as semi-transparent were subsequently converted to the active transparent wrapper (e.g. Fidelity converted two of its semitransparent ETFs earlier this year). Indeed, the vast majority of assets and inflows in active ETFs are in transparent active funds (i.e. those that disclose portfolio holdings at T+1), demonstrating that portfolio transparency need not be an impediment to the success of an active ETF strategy. However, non-transparent structures continue to see periodic interest from fund managers who want to shield their intellectual property on some flagship active strategies.

Option-based ETFs

ETFs fuelled by options have also growing fast ever since the SEC’s 2020 ‘Derivatives Rule’. By setting leverage limits and risk management standards, the rule actually it easier for ETFs to employ derivatives-based strategies.

As a result, the assets of US option-based ETFs have grown about 600 per cent over the past three years to $115bn, according to JPMorgan. Of this, well over half are call-put writing ETFs, followed by “buffer ETFs”, which make up just over a third of the assets. The remainder is a motley variety of other option-based strategies, like 0DTE funds and structured product replication.

As FTAV has written before, these option ETFs are just a subset of a broader and growing universe of funds that derive income from writing options, which some people think is suppressing volatility.

FWIW, Kolanovic and Kaplan agree that they are a “major driver” of becalmed Vix, but don’t think they’re as dangerous as the previous short-Vix ETFs that blew up in 2018.

With the large amount of volatility selling by these overwriting ETFs, some have drawn comparisons to 2018’s Volmageddon episode, when large volatility selling flows via inverse VIX ETPs initially suppressed volatility, but ultimately led to a volatility spike and collapse of the short vol strategy itself. However, for overwriting ETFs we don’t see a similar mechanism at play that could produce a Volmageddon-type episode since the call overwriting strategies are unlevered and have no need to sell equity exposure as the market declines. That said, the price range over which these ETFs suppress volatility is relatively narrow. If the market sells off by ~5-10%, the volatility suppressing force from these strategies largely disappears, leaving markets more vulnerable to other selling flows.

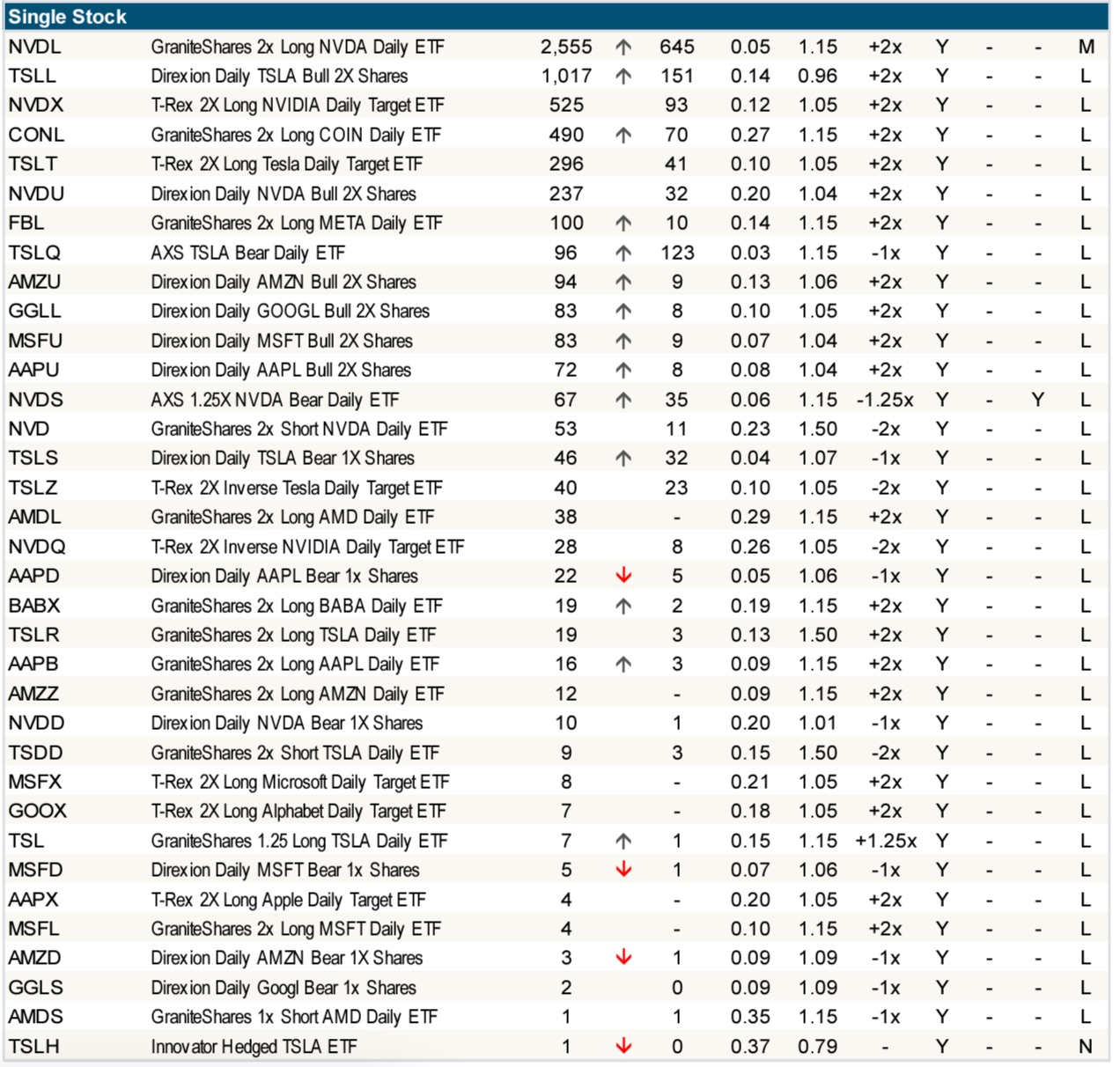

Single-stock ETFs

Since the SEC first waved them through in July 2022 we’ve also seen a growing number of single-stock ETFs, which typically use derivatives to make it easy for investors to go short or gain leveraged exposure to companies like Tesla, Alibaba, Coinbase and Nvidia.

You might say these are a naked corruption of the original purpose of ETFs designed only to give easy access to leverage to traders who probably shouldn’t have it, but we couldn’t possibly comment. Here’s a list of some of them.

At the moment there are about 60 single-stock ETFs listed in the US, which have cumulative assets of $8.7bn (the vast majority is in Tesla and Nvidia ETFs). This is obviously tiny compared to the overall industry, but these are trading tools for day trades — who go in and out opportunistically — so AUM is a poor measure of their overall impact.

As JPMorgan’s Kolanovic and Kaplan point out, the dynamics of daily rebalancing in derivatives mean that they are inherently procyclical trading tools that can cause problems if they grow too large. FTAV’s emphasis below:

An advantage is that losses to investors in these ETFs are limited to their initial investment, while other forms of leverage could deliver losses exceeding 100% (e.g. by short selling a stock that more than doubles or borrowing 50% reg T margin to go long a stock that falls by 50%+). However, because levered ETFs deliver daily leverage, they underperform during mean-reverting markets and outperform during trending markets due to the daily leverage resets and compounding of returns . . . Additionally, levered ETFs rebalance in a short gamma fashion (i.e. they have to buy the underlying on up days and sell it on down days), which can exacerbate volatility on their target stocks should these products gain material assets.

ETF options

On top of all this, there is a growing ecosystem of options written on ETFs themselves. The outstanding volume of US ETF options now comfortably above $600bn, up from well under $200bn five years ago.

Which means that after being briefly leapfrogged by single-name equity options in the 2020-21 retail trading mania, ETF options are once again the second-largest segment after index options (which are in turn increasingly dominated by zero-day options).

At least here there is little change in terms of diversity. The upswing is mainly caused by a huge increase in trading options on SPY, State Street’s flagship S&P 500 ETF.

SPYs average daily notional option trading volumes have tripled just since 2021, to reach $409bn this year, about two-thirds of the total, according to JPMorgan.

Options on SPY, the Nasdaq QQQ ETF and BlackRock’s Russell 2000 small-caps ETF together account for about 95 per cent of all ETF option volumes this year. JPMorgan notes that most of the ETF options being traded are puts, so these are probably mostly options used to hedge an overall portfolio

Finally, there’s the emergence of crypto ETFs over the past year, which are too tedious to spend even more time on. But they add another dumb aspect to the ETF universe’s increasing complexity.

People continue to freak out about the growth of passive investing, often for misguided or self-serving reasons. If they really want to find out where the next market stupidity is going to come from, then the parallel growth of gimmicky, derivatives-based and/or complex ETFs is a much better place to look.

{kind=link}